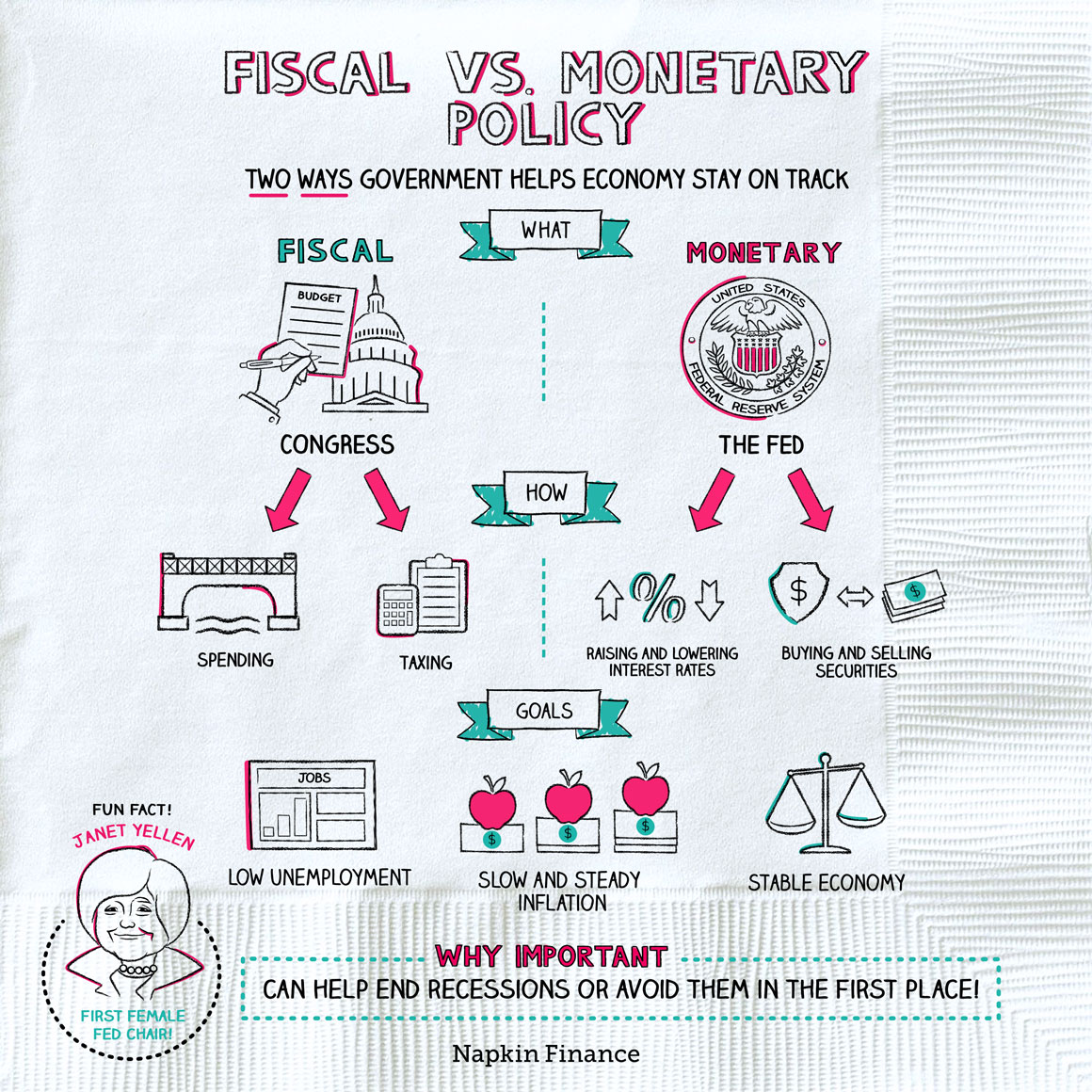

26 Sep Which double taxation is the double-edged blade out of fund

The example in Contour step 1 portrays this aspect. Triplets James, John, and you may Jack graduate college and check out run an equivalent company, nevertheless the three employ additional old-age discounts methods. James sets $2,100 a year of many years twenty-five-65 into their house safer. John invests $dos,100 per year from years 25-forty five immediately after which closes. Jack spends $dos,000 a-year toward getaways for 2 decades immediately after which invests $dos,100000 a year out of age forty-five-65. Both Jack and you will John receive six.5% desire compounded a year. Just what will their retirement funds feel like once they every retire within age 65?

Figure 2 shows the way the exact same investment off $2,000 expands more an excellent 10 to thirty year months with yields anywhere between four to help you nine per cent.

For many who subscribe to their 401(k) plan on a great pre-tax basis or take that loan out of your membership, you’re paying oneself right back with the an afterwards-income tax base

6. Money during the an effective 401(k) package may be a double-edged sword. After you retire and distribute your bank account, you’ll have to shell out taxation once more.

If you cancel a job which have a great loan, when you find yourself your account equilibrium is generally permitted stay-in this new package, your loan have a tendency to default if you fail to afford the count inside the full ahead of the prevent of elegance months.

You will want to remember that removing your difficult-acquired funds from your 401(k) bundle decreases the period of time those funds will be accruing money and you will compounding attention. Please make sure to look at the outcomes in advance of asking for a loan out of your 401(k) account.

7. You do not be eligible for all your account balance in the event the your terminate or take a delivery. Whenever you are any cash deferred from the payment is always a hundred% your own for people who get off the firm, employer contributions could be at the mercy of a great vesting agenda. What is an excellent vesting plan? A great vesting plan lies out the number of https://paydayloancolorado.net/towner/ years in which you should be involved in purchase to earn full control off those people workplace efforts. Different types of boss benefits may be subject to different vesting schedules. A quite common exemplory instance of a vesting schedule ‘s the half dozen-seasons graded vesting plan, shown in the Contour step three below. Just what this plan function is that you need certainly to functions half dozen years to help you attain full ownership of manager efforts on your account. For individuals who terminate a position that have less than six many years of provider you will be eligible to the new related vested percent nevertheless remaining membership would-be forfeited back into the new employer.

Additionally, by firmly taking financing and are also incapable of shell out it back during the detailed period of time, your loan becomes a premature shipping, taxable in the loan goes into default, and may even getting at the mercy of an extra 10% for the punishment fees

When you are being unsure of in case your workplace efforts was at the mercy of good vesting schedule otherwise should your package has the benefit of 100% instantaneous vesting, you should consult with your realization package malfunction.

8. 401(k) account was mobile. If you have several 401(k) account, you can consolidate your accounts of the swinging (otherwise running more) the new account together with your earlier boss into the this new employer package. Rolling more the account works well since it enables you to flow your bank account regarding prior employer’s package as opposed to incurring one shipments punishment.

nine. 401(k) preparations would be impacted by income tax reform. About wake of one’s previous election, the news has been littered with headlines centered doing income tax change. Releasing rumors speculate your purpose of new U.S. Congress within the 2013 is always to cure otherwise dump income tax deductions and you can slice the deficit. I know you are considering these deduction cutbacks commonly mostly affect employer-sponsored healthcare and will not mean one thing for your 401(k), but you one to 401(k)s was adversely affected by tax reform in earlier times.

No Comments