20 Sep seven an effective way to funds a cellular, are designed, otherwise standard house

- Cellular domestic compared to. were created family compared to. standard family

- 7 a method to money a plant-generated household

Insider’s masters select the right products and services to manufacture wise conclusion with your currency (this is how). Sometimes, we found a payment from our all of our partners, however, the opinions try our own. Words apply at even offers noted on these pages.

- Cellular, are formulated, and modular property is actually similar, however, discover key differences that may affect the investment offered.

- Of several applications need to have the the home of has at the least 400 square legs off living space.

- Dependent on your position, an unsecured loan is a far greater alternatives than just property financing.

- Read more stories out of Personal Financing Insider.

Cellular land is actually a far greater fit for particular homebuyers than conventional house. You really have a lower budget, require an inferior room, or need certainly to disperse our home afterwards.

Mobile household versus. are manufactured house against. modular home

The newest words « mobile home, » « are produced home, » and you may « modular family » are utilized interchangeably, however, you will find some key variations. Additionally the style of that you choose should determine the kinds of mortgage loans you could come across to finance the purchase of just one.

All the around three are made when you look at the a manufacturing plant and you will delivered to the newest website, whereas antique house is actually constructed close to the house or property.

Cellular belongings and you will are formulated land are extremely equivalent during the build and you can physical appearance. An element of the difference between him or her is when they certainly were made. People depending in advance of June 15, 1976, are known as cellular residential property, when you find yourself those individuals dependent immediately after after that are known as were created house.

Manufactured home also are founded considering cover conditions set from the brand new Company out of Homes and you will Metropolitan Developement (HUD). That is the main distinction among them and you may modular residential property, and this follow cover requirements managed by the local or state government.

seven an approach to money a factory-made house

You really have a number of options to own loans dependent on your downpayment, credit rating, and measurements of the home. The best complement may also get smaller to help you if you would like a cellular, are created, otherwise modular house.

step one. Federal national mortgage association

The new Fannie mae MH Virtue Program is for are manufactured belongings. You will get a 30-year fixed-rate financial, and therefore program even offers down rates towards are manufactured home loans than you possibly might discover somewhere else.

You desire a great step three% downpayment and at the very least an effective 620 credit history. Our home as well as need fulfill particular requirements – particularly, it ought to be minimum a dozen feet large and also 600 rectangular legs of liveable space.

dos. Freddie Mac computer

Freddie Mac even offers finance having are created property, and you may choose from many different repaired-price and you can variable-rates terms and conditions. Such as Federal national mortgage association, Freddie Mac requires the the place to find fulfill requirements. The house need to be at the very least several base greater that have eight hundred sqft regarding liveable space.

3. FHA financing

You can get an FHA loan to own sometimes a made or modular family. You get a keen FHA financing as a consequence of a classic lender, but it is backed by new Government Property Government.

Name We finance are used to get a home but not the belongings they consist for the. The amount you could borrow depends on which type of property you are to acquire, it keeps apparently reduced borrowing from the bank restrictions. A subject We loan was a good idea if you find yourself working with an inferior funds.

Name II fund are widely used to buy both domestic and you may the new land underneath. The house or property need to meet specific conditions, eg which have eight hundred sqft out of living area.

Note: You can purchase an enthusiastic FHA are built home loan which have a card get only 580 and you may good step three.5% advance payment. You might be accepted that have a credit score as low as five hundred, nevertheless the tradeoff is that you must have an effective 10% down payment.

4. Va funds

Fund backed by new Service out-of Experts Items are having being qualified productive military members, pros, and their family. You should use a great Va mortgage buying a made otherwise modular family.

You do not have a downpayment should you get a Va loan, additionally the lowest payday loans Sedalia credit rating necessary varies according to hence bank you employ.

5. USDA finance

You should use financing supported by the us Department regarding Agriculture to acquire a made otherwise standard domestic. Our home should have about 400 sq ft off living space, and it also should have started built on or shortly after .

Just as in a Virtual assistant loan, you don’t need a deposit, and the credit rating need is dependent upon the lending company.

Note: USDA finance are to own house inside rural parts, while have to have a minimal-to-modest money in order to qualify. Maximum income level hinges on where you live. You can view your own county’s earnings limitation right here.

6. Chattel money

Chattel fund are sort of money for various brand of qualities, in addition to vehicles and ships. You are able to an excellent chattel financing to acquire a mobile, are available, otherwise standard house.

These types of fund has high interest rates versus other sorts of money on this checklist, along with shorter name lengths. But a beneficial chattel mortgage could well be advisable for those who cannot be eligible for other types of lenders, or you know you need a cellular family as opposed to a manufactured otherwise standard home.

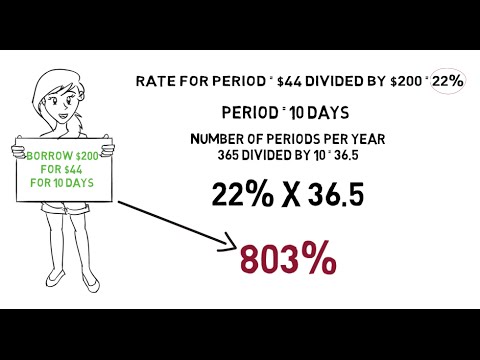

7. Signature loans

Loan providers place restrictions precisely how you are able to money from a great personal loan. Dependent on and therefore bank you utilize, you may capable put the money with the a cellular, are made, otherwise modular house.

A consumer loan can be cheaper upfront than just a home loan, because you won’t have to buy really settlement costs. Signature loans constantly charge higher rates than simply lenders, though, especially if you has actually a dismal credit get.

To choose ranging from these cellular home loan selection, consider which kind of house we would like to purchase. Following discover hence applications you be eligible for.

No Comments